Protecting All That is Green: Integrating Nature into Carbon Markets to Drive Conservation

By Joshua Cohen

In 2025, an area of approximately 50 times the size of New York City was lost to forest fires in the Amazon Rainforest. The carbon market in the Amazon currently stands at over $200 million USD—when those credits went up in smoke, the actual benefits lost by the Amazonian communities far exceeded the value of the carbon abated by the trees.

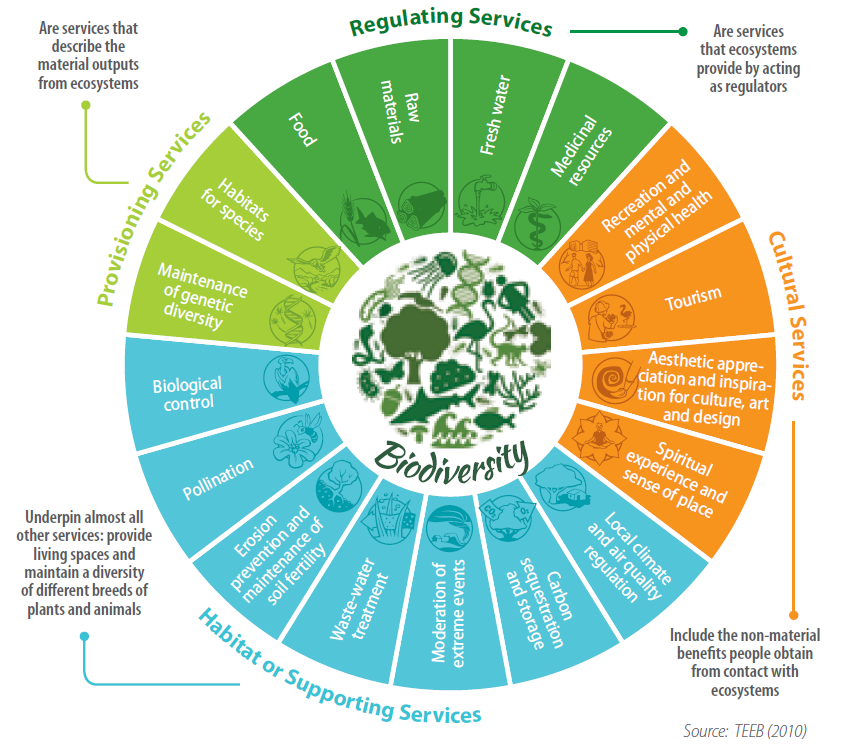

Ecosystem Services. Source: Global Youth Biodiversity Network (2016) CBD in a Nutshell. Global Youth Biodiversity Network. Germany, 204 pages. Reproduced with acknowledgement.

Carbon markets, through the trading of carbon credits, represent a key mechanism to finance climate mitigation projects. In the valuation of any project, only the credits generated by the net carbon abated are considered. While this computes the environmental benefits of many types of projects, such as energy efficiency, it omits the co-benefits to nature for many types of land-use projects, such as reforestation, afforestation, and avoided deforestation. These benefits are also known as ecosystem services and include the improvement of air and water quality, soil erosion prevention, and biodiversity maintenance. The price of credits generated by these projects for carbon markets should incorporate both the value of the abated carbon and the ecosystem benefits that the implementation of these projects provides.

By integrating the value of ecosystem services into these credits, the price of the credits would increase for all land-use projects. The value of each credit would not only count the carbon abated but also the ecosystem services provided. This makes project development of all land-use projects more financially viable but has a particularly large impact on potential projects where the ecosystem benefits would be high and the climate benefits would be marginal. Given that global biodiversity finance comprises 10% of climate adaptation finance, this integration represents a chance to use climate finance flows to “double dip” and incur benefits to ecosystems as well.

Beyond the scale of investments in carbon markets, it would also change the type of projects that are developed. When ecosystems are considered, projects that abate additional carbon but have harmful effects on biodiversity and nature would be deprioritized. Projects such as hydropower dams, which have generated 30% of all credits under the Clean Development Mechanism (CDM), incur damages to freshwater ecosystems and hurt the fish yields of communities around the dams. While hydropower is valuable in transitioning away from fossil fuels, markets should be used to encourage projects with as few downsides as possible that would otherwise struggle to catalyze capital—the non-use value of land is often not sufficiently economical to avoid being slashed, burned, and turned into agriculture without markets to preserve them.

Climate activists have traditionally resisted integrations such as these, fearing that the focus on nature-related initiatives would limit the carbon abatement goals and weaken the effect that carbon markets have in raising capital for climate change action. This perspective loses sight of the big picture of environmental action—climate change mitigation is ultimately intended to preserve our biosphere and our planet. As of 2025, seven of the nine planetary boundaries have been breached. Integrating nature credits and allowing the catalyzation of finance is vital to protect these other necessary boundaries, such as biodiversity integrity, nitrogen and phosphorous flows, and land use change.

Prices of nature credits vary greatly—from $7 USD/ha to $68,000 USD/ha; low or uncertain prices can both be deterrents for investors. Corporate purchasers of traditional carbon credits, such as airlines, have traditionally responded to public pressures for remediation for the climate damages that they have caused. The same pressure does not exist for nature credits. At its current rate, global demand for biodiversity credits is expected to reach $2 billion USD by 2030. This is approximately 10% of the expected size of the voluntary carbon market. However, top-down initiatives, such as those from the EU, as well as increased awareness of biodiversity issues can drive increased demand beyond those estimates. Even if the market for biodiversity credits does not grow beyond current estimates, a marginal project introduced now would be issued with comparatively more credits than they otherwise would have been—a small change, but one that is still worth pursuing.

Nature, biodiversity, and carbon credit markets will continue to grow on their own. To ensure that the finance flowing into these markets is as effective as possible at achieving environmental outcomes, these markets need to be integrated. It may not unilaterally restore our planetary boundaries which have been crossed, but it would be an incremental step in the right direction.

Joshua Cohen is a BA/MALD student in his final year at Tufts University. Josh is currently a research assistant at the Fletcher School’s Center for International Environment and Resource Policy (CIERP) with both the Climate Policy Lab and the Shared Waters Lab. His academic interests focus on the intersection of environmental and international legal issues, especially with regards to marine and freshwater issues.